TMRRO - Tactical Macro-Market Regime Risk Overlay

You keep your models. We tell you when the regime is changing.

TMRRO is a monthly macro-risk intelligence layer that sits on top of any portfolio strategy. It delivers a clear Equity Market Regime Risk outlook — Bullish or Bearish and individual asset class ratings, so you know where to express the posture. No new models. No outsourcing. No disruption to your investment philosophy.

A CIO-quality regime framework. Flat-fee pricing. Yours to implement, in full discretion

What TMRRO delivers each month?

Every month, ACQM publishes three outputs that translate complex macro conditions into clear, actionable guidance:

Equity Market Regime Risk Rating— A top-level posture on US equity risk: Bullish or Bearish. Derived from ACQM's proprietary market model assessing sentiment and volatility conditions.

Asset Class Ratings— Overweight, Neutral, or Underweight ratings across major asset classes (US large cap, US small cap, international equity, investment-grade bonds, high-yield bonds, gold, and commodities). These are derived from our proprietary macro model (assessing economic cycle, monetary policy, and liquidity regimes). They tell you where to express the regime posture within your existing portfolio structure.

Monthly Regime Risk Report— A structured implementation document that translates the ratings into practical guidance for 60/40 and diversified portfolios, including documented decision rationale to support compliance review.

The problem with static portfolios in a dynamic world

Markets don't move in straight lines. They rotate through expansion and contraction, inflationary and disinflationary regimes, liquidity abundance and liquidity withdrawal, risk-on and risk-off cycles.

Yet most advisory portfolios are constructed and left as if conditions are static. When the regime shifts, the questions come fast:

"Should we reduce equity exposure right now, or is this just noise?"

"Which asset classes look strongest in this environment?"

"Is this a risk-on or risk-off period and how do I explain my position to a client if I'm wrong?"

"Am I making this call on data or on anxiety?"

Without a structured, rules-based framework, tactical decisions become subjective, narrative-driven, and inconsistent. That inconsistency is exactly what erodes client confidence and advisor credibility over a full market cycle.

Why most approaches leave something on the table?

Most advisors navigate this challenge one of three ways and each comes with a meaningful limitation:

Static 60/40 or diversified ETF models— Periodic rebalancing, minimal tactical adjustment. Disciplined and low-cost, but entirely regime-blind. When conditions shift materially, the portfolio doesn't respond.

Outsource to a TAMP or model marketplace— Delegate the allocation decisions to a third party. Convenient, but at the cost of internal investment differentiation, AUM-based margin compression, and meaningful control over the process your clients associate with your name.

Discretionary tactical calls— Reduce equity after a correction, increase risk when sentiment improves, follow a strategist view. The intent is right; the problem is structural. Without a documented, repeatable framework, these calls are reactive, hard to justify in compliance reviews, and inconsistent over time — even when individually correct.

TMRRO was built to fill the gap that all three approaches leave open: objective, systematic regime intelligence that integrates into your existing process without replacing it.

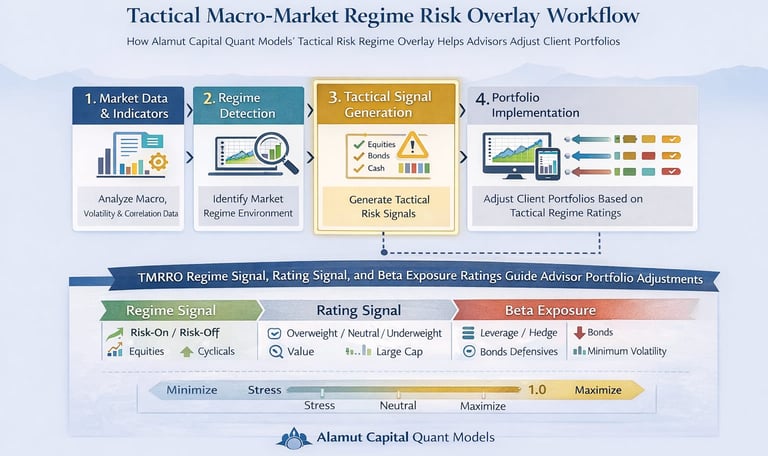

How TMRRO Works

TMRRO is an overlay, not a replacement. It doesn't change your portfolio models, your investment philosophy, or your client relationships. It adds a structured, rules-based decision layer that sits on top of whatever you're already doing.

Each month, our proprietary quantitative framework synthesises three categories of inputs:

Economic cycle assessment— Growth and inflation indicators: consumer demand, employment trends, wage dynamics, and inflation trajectory

Monetary policy and liquidity— The direction and intensity of rate and liquidity conditions, including yield dynamics and central bank policy posture

Sentiment and volatility regime— Measures of risk appetite, positioning, and volatility that signal stress, crowding, or regime inflection points

These inputs are synthesised into two outputs: an Equity Market Regime Risk rating (Bullish, Bearish, or Neutral) and supporting asset class ratings (Overweight, Neutral, or Underweight). Together, they answer the two questions that matter most during regime transitions: how much equity risk should we be carrying, and where should we be carrying it?

How Advisors Benefit?

Investment practice benefits:

Make allocation adjustments with discipline and documented rationale not instinct.

Add meaningful risk management to low-cost index ETF portfolios without switching to active management.

Support client conversations with data and a clear framework, not opinions and market commentary.

Demonstrate a more institutional, process-driven approach to portfolio oversight.

Commercial and structural benefits:

CIO-quality macro intelligence at a flat fee not an AUM percentage that compounds against your margin as you grow.

Fully white-labeled: your clients see your brand, your process, your name.

No disruption to existing custodial relationships, models, or portfolio architecture.

TMRRO is a fit if...

TMRRO is designed for independent advisors and RIAs who want to bring systematic, regime-aware risk management into their practice without replacing their existing portfolio structure or outsourcing their investment decisions.

It's likely a strong fit if:

You run low-cost index or ETF-based portfolios and want a disciplined risk management layer that limits drawdowns without going fully active.

You make tactical allocation decisions today but they're based on market commentary rather than a documented, repeatable framework.

You want to be able to explain every allocation shift to clients and compliance with clear, data-backed rationale.

You want to stay in full control of your investment process while adding institutional-grade macro intelligence to your decision-making.

You believe that protecting clients from severe drawdowns, not just chasing returns is what makes compounding work over a full market cycle.

If you're already running a proprietary quantitative process with dedicated research resources, TMRRO is likely redundant. It's built for advisors who want to access that capability without building it in-house.

Contact Us

models_solution@acquantmodels.com

© 2026. All rights reserved.

Disclaimer: The model portfolio strategies provided by Alamut Capital Quant Models Inc. are offered solely to registered advisers and are licensed as intellectual property. We do not provide personalized investment advice, portfolio management services, or recommendations to any individual investor.

The information provided is not intended to be and does not constitute financial, legal, tax, or investment advice. Implementation of any model strategy is the sole responsibility of the subscribing advisor or portfolio manager, who must determine its suitability and compliance with their clients’ investment objectives, risk profiles, and regulatory obligations.

Alamut Capital Quant Models Inc. is not registered as an investment adviser in any jurisdiction and does not interact with any investors. The firm does not offer account-level services, make investment decisions on behalf of clients, or assume discretionary authority over assets.

Past performance is not indicative of future results. All investments involve risk, including possible loss of principal. Use of our models does not guarantee any specific outcome or performance.

Alamut Capital Quant Models Inc

Get in touch with us to inquire about our Quantitative Investment Solutions and demo of our strategies

Kitchener, Ontario, Canada