40+ Regime-Aware Model Strategies.

ACQM's model portfolio strategies give independent advisors access to a quantitative, regime-aware investment process across five risk tiers and four strategy categories so you can serve a wider range of client mandates with the discipline and depth of an in-house CIO team.

Built to adapt when markets change, not just when calendars roll over.

Flat-fee access. White-labeled. Implemented through your existing custodians. You keep full control.

Five Risk Tiers. Four Distinct Categories

The Strategy Library — Four categories. Five risk tiers. One systematic framework

All ACQM model portfolios are built on the same quantitative, regime-aware foundation — but organized into four distinct categories to serve the different constraints and objectives advisors actually work with:

Core Strategies— The flagship multi-asset model portfolios. Systematic, regime-aware allocation, built for advisors who want a disciplined primary investment process with adaptive risk management at the center.

Compliance-Lite Core Strategies— The same systematic framework as Core, constructed with a streamlined security set designed to reduce compliance review burden. Purpose-built for advisors and firms operating under tighter product shelf or due-diligence constraints.

Tax-Efficient Strategies— Regime-aware portfolio construction with an explicit after-tax objective. Designed for advisors managing taxable accounts where minimizing realized gains and tax drag is a priority alongside risk management.

ETF Strategies— Systematic, regime-aware model portfolios built entirely with exchange-traded funds. Transparent and compatible with advisors who run passive or index-based investment philosophies and want to add a risk-management overlay without going to individual securities.

All four categories are available across five risk tiers — Adventurous Growth, Aggressive Growth, Moderate Growth, Conservative Growth and Preservation Growth — giving advisors the flexibility to match strategy to client mandate rather than forcing a client into a strategy that doesn't fit.

How the models are built — and what makes them different

Most model portfolios are constructed once and rebalanced periodically. They're designed for a world where market conditions are stable and drift is the primary risk to manage.

ACQM's models are built on a different premise: that market regimes, the underlying conditions driving equity performance, asset class correlations, and risk appetite, change materially over time, and that a portfolio which ignores those shifts will systematically take on more risk than the advisor or client intended.

Every strategy in the ACQM library is built on the same systematic, quantitative process:

Regime-aware construction— Allocations are informed by the prevailing macro-market regime, not just long-run return assumptions. When conditions favor risk, the portfolio is positioned to participate. When conditions deteriorate, risk is reduced proactively rather than reactively.

Downside minimization as a design principle— Every strategy is built with explicit attention to drawdown reduction. The goal is not to maximize return in isolation, but to deliver better risk-adjusted outcomes over a full market cycle which ultimately supports the compounding process and client retention.

Systematic and rules-based execution— Portfolio decisions follow a disciplined, repeatable process grounded in quantitative data. This removes the emotional and narrative-driven decision-making that characterizes many reactive approaches, and gives advisors a defensible, documentable rationale for every allocation.

Multi-asset breadth— Depending on category, strategies span US equity, international equity, fixed income (investment grade and high yield), gold, and commodities, giving the framework real diversification levers to work with across different regime environments.

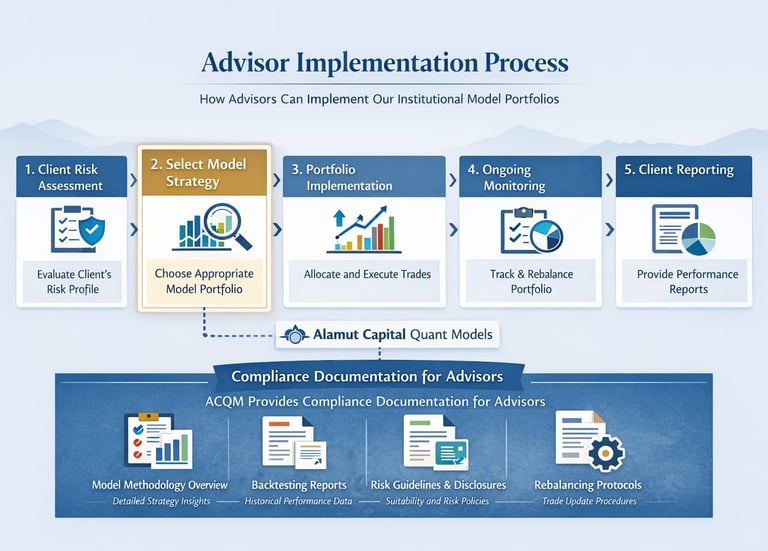

How advisors put ACQM models to work

Implementation is designed to fit your existing process, not replace it. You don't need new custodians, new platforms, or new workflows.

Step 1 — Map client risk profiles to our five tiers. Adventurous Growth, Aggressive Growth, Moderate Growth, Conservative Growth and Preservation Growth. Use your existing risk assessment process; the five tiers are designed to align with standard advisory practice.

Step 2 — Select the appropriate strategy or strategy mix. Choose from Core, Compliance-Lite, Tax-Efficient, or ETF categories based on client constraints, account type, and your firm's product shelf. You can implement a single strategy per client or blend across strategies.

Step 3 — Receive the monthly model update. Each update includes the full holding list with ticker symbols and allocation weights, an effective date, and any changes from the prior period. Updates arrive in a format ready to import into your trading system.

Step 4 — Implement through your existing setup. Apply the model allocations directly in client accounts via your custodian (Charles Schwab, Interactive Brokers, Altruist, and others) or trading platform (iRebal, Orion Eclipse, Black Diamond, and more). No new infrastructure required.

Step 5 — Review the ongoing performance summary. Monthly performance context and regime commentary keeps you informed and gives you the narrative for client conversations without requiring you to do the research yourself.

You retain full discretion over every implementation decision. ACQM provides the framework and the signals; you apply them within your client-specific constraints, IPS guidelines, and suitability requirements.

Contact Us

models_solution@acquantmodels.com

© 2026. All rights reserved.

Disclaimer: The model portfolio strategies provided by Alamut Capital Quant Models Inc. are offered solely to registered advisers and are licensed as intellectual property. We do not provide personalized investment advice, portfolio management services, or recommendations to any individual investor.

The information provided is not intended to be and does not constitute financial, legal, tax, or investment advice. Implementation of any model strategy is the sole responsibility of the subscribing advisor or portfolio manager, who must determine its suitability and compliance with their clients’ investment objectives, risk profiles, and regulatory obligations.

Alamut Capital Quant Models Inc. is not registered as an investment adviser in any jurisdiction and does not interact with any investors. The firm does not offer account-level services, make investment decisions on behalf of clients, or assume discretionary authority over assets.

Past performance is not indicative of future results. All investments involve risk, including possible loss of principal. Use of our models does not guarantee any specific outcome or performance.

Alamut Capital Quant Models Inc

Get in touch with us to inquire about our Quantitative Investment Solutions and demo of our strategies

Kitchener, Ontario, Canada